As Featured In

Your 2025 Tax Bill Is About To Hit. But Your 2026 Strategy Starts Now. Join The 3-Day Challenge Where...

Not Learn About It, Actually Build It.

(4,400+ high-income earners used this system to stop losing money to taxes and start building real wealth.)

Mar 20th - Mar 22nd | 10 AM - 4 PM EST

Offer Ends Soon

Real People. Real Numbers.

$125K/year

Year 1 Value

$61K - $109K

She was losing $1,237 every single month to a W-4 she filled out in 2019. That's $14,840/year, gone before she saw it.

But that was just the first leak.

Her wealth plan identified 6 strategies she qualified for but wasn't using:

The STR strategy alone, with only 3-5 hours per week to meet material participation, created more tax savings than most people's entire annual contribution to their 401(k).

Week 1: Adjust W-4, increase 401(k) contributions. Week 2: Set up investment accounts. Week 3-4: Begin STR market research. 90 days to first property cash flow.

$180K combined

Year 1 Value

$18.5K - $43.5K

His CPA files taxes every year. Does a good job. Never misses a deadline.

But there's a gap between "filing" and "optimizing."

When's the last time your CPA called you in June and said "you have $43,000 exposed here, let me show you how to keep it"?

That call never comes. Because that's not their job. CPAs file. They don't plan.

Chad's wealth plan mapped 8 strategies to his income:

Each strategy had a dollar value. Each had an implementation week. Each had the documentation required.

$300K combined

Year 1 Value

$86K - $192K

They didn't want vague promises. They wanted the exact math.

Not "you could save money." Not "this works for most people."

They wanted to see where every dollar comes from. Line by line. Strategy by strategy.

At $300K combined income in San Francisco, they're in the 46% combined bracket. Every dollar of deductions saves 46 cents. That math changes everything.

Their wealth plan identified 8 strategies totaling $86,220-$192,050 in year-one value:

Plus: 529 plan structure for their 9-month-old. Revocable living trust to protect assets. 75% Bitcoin allocation strategy with custody progression.

$250K/year

Year 1 Value

$55.9K - $68.3K

He'd researched for years. He knew about S-Corp elections. Solo 401(k)s. Augusta Rule. Cost segregation.

He didn't need more information. He needed a sequence.

Do this Monday. Do this Wednesday. Apply here Thursday. Wait 14 days. Then do this next.

The order matters more than the strategies. Wrong order can cost you. Right order creates immediate results.

His wealth plan broke it into a 30-Day Launch Checklist:

Week 1: Schedule CPA consultation for S-Corp election timing. Determine Q2 vs Q3 start date. Review PLLC operating agreement.

Week 2: Create Accountable Plan documentation. Measure home office. Install vehicle tracking app.

Week 3: Increase Bitcoin DCA to $1,365/month. Open Solo 401(k). Review brokerage for tax-loss harvesting.

Week 4: Research STR market. Connect with property owners. Launch cohosting outreach.

$150K/year

Year 1 Value

$28K - $62K

She was paying $43,000/year in taxes. After restructuring: $28,500.

That's $14,500 back every single year.

But here's what made her plan different: she had almost no liquid capital to deploy. $0-$2,000 available. $50K+ in non-mortgage debt. Cash flow matching expenses with nothing left over.

Most advice assumes you have money to invest. She needed strategies that cost nothing to implement.

Her wealth plan prioritized zero-capital moves first:

All strategies above cost $0 to implement.

Then the plan showed her how to use those tax savings to fund the next phase: cohosting (manage others' STR properties for 20-25% revenue share, zero acquisition cost), projected at $3,000-$12,000 year-one profit.

30-Day Launch Checklist: Week 1: Confirm LLC, open business checking, sign Accountable Plan. Week 2: Augusta Rule calendar, home office documentation. Week 3: W-4 adjustment, Solo 401(k) setup. Week 4: First cohosting outreach.

*Year 1 Value includes estimated tax savings, cash flow improvements, and tax-advantaged contributions based on each person's income, filing status, and marginal tax bracket. Individual results vary based on your specific situation.

Different situations. Different numbers. Same process.

One of these will click for you. Then you'll know exactly where to focus.

See The Process Inside The ChallengeSuccess Stories

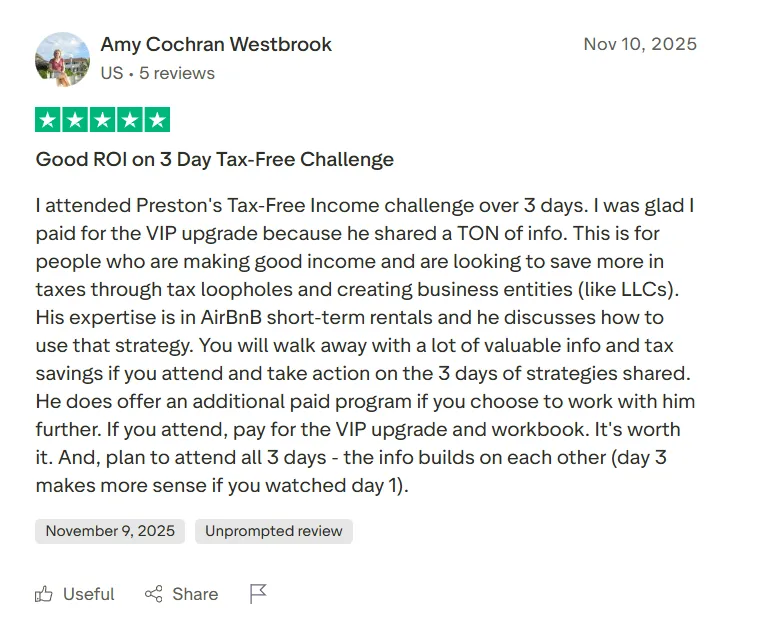

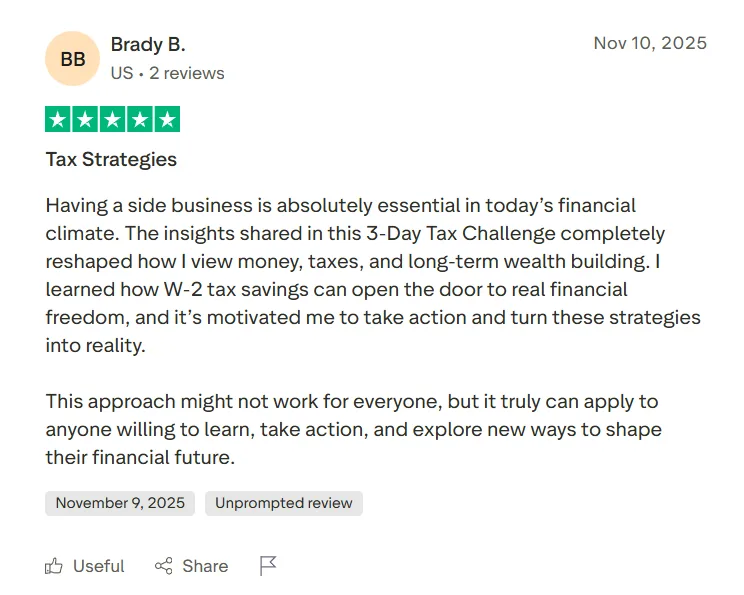

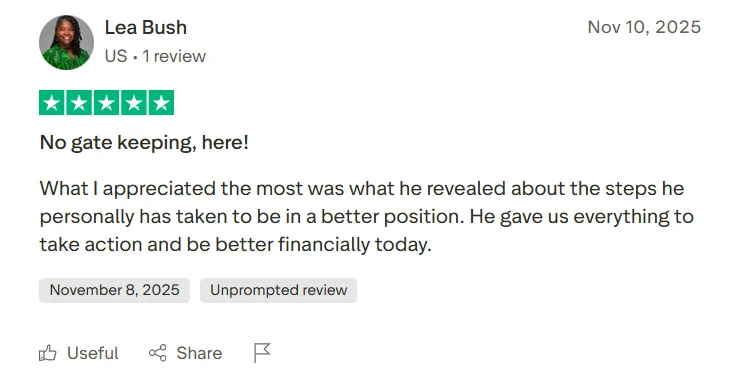

"We're both full-time & have a daughter. We didn't wanna just stumble around in the dark. If you wanna get out of the 9-to-5, here's how to do it. It's such a blessing."

"When we talk about Preston doing an absolute masterclass on how to do this... I couldn't give it a bigger endorsement. It's about as legit as it gets."

"I've never been someone who just 'gets it' the first time. It has been leaps and bounds, and worth it. Every step is well thought out."

Verify It Yourself

Here are 3 things you can verify right now, depending on your situation:

If you're W-2:

Pull up your most recent paystub. Find your federal withholding. Multiply by your pay periods. Compare to your actual tax liability from last year's return. If there's a gap, that's cash flow you're giving away interest-free.

If you own a business or have 1099 income:

Are you operating as a sole proprietor or single-member LLC paying 15.3% self-employment tax on all your profit? An S-Corp election splits income into salary and distributions. Distributions aren't subject to SE tax. The math is specific to your income, but the gap is usually $4,000–$10,000+ annually.

If you have business expenses:

Home office. Vehicle mileage. Phone and internet. Equipment. Each has a specific deduction value based on your usage. Most people leave $2,000–$6,000 on the table annually because they don't track it correctly or don't know the documentation requirements.

That's a free lesson. If any one of these applies to you, you just found $2,000–$10,000. That alone pays for this event 50x over.

These are 3 of the 40+ strategies we cover. The challenge shows you which ones apply to your income and in what order.

Every guru online says the same thing. You've heard it all. And it's not that you don't get it... It's just not practical when you're actually trying to do it.

Every raise comes with a bigger tax bill. You work more, earn more, and end up with less.

Big financial goals keep getting pushed back because there's never "enough" to start.

Every money decision feels like a coin flip. Pay off debt or invest? Max out 401k or save for a rental?

You're hoping it'll work out instead of KNOWING it will.

We're not going to give you theory. We're going step by step. Detailed how-to. Not more Rich Dad Poor Dad advice. Actual implementation.

The Journey

Hi, my name's Preston. I was in my 20s doing everything "right" with money but getting nowhere.

I was living with my wife in my parents' basement as I was struggling with money at that time. My wife Bridget was working long shifts as a respiratory therapist. I was in sales.

We were both doing what we thought we were "supposed to do" but somehow still feeling financially stuck.

None of this means you lack discipline or intelligence. It just means... You're Doing What Everyone Else Does With Money. So, you also struggle like everyone else.

Until... we started learning everything we could about how money really worked. We changed the plan and...

The System

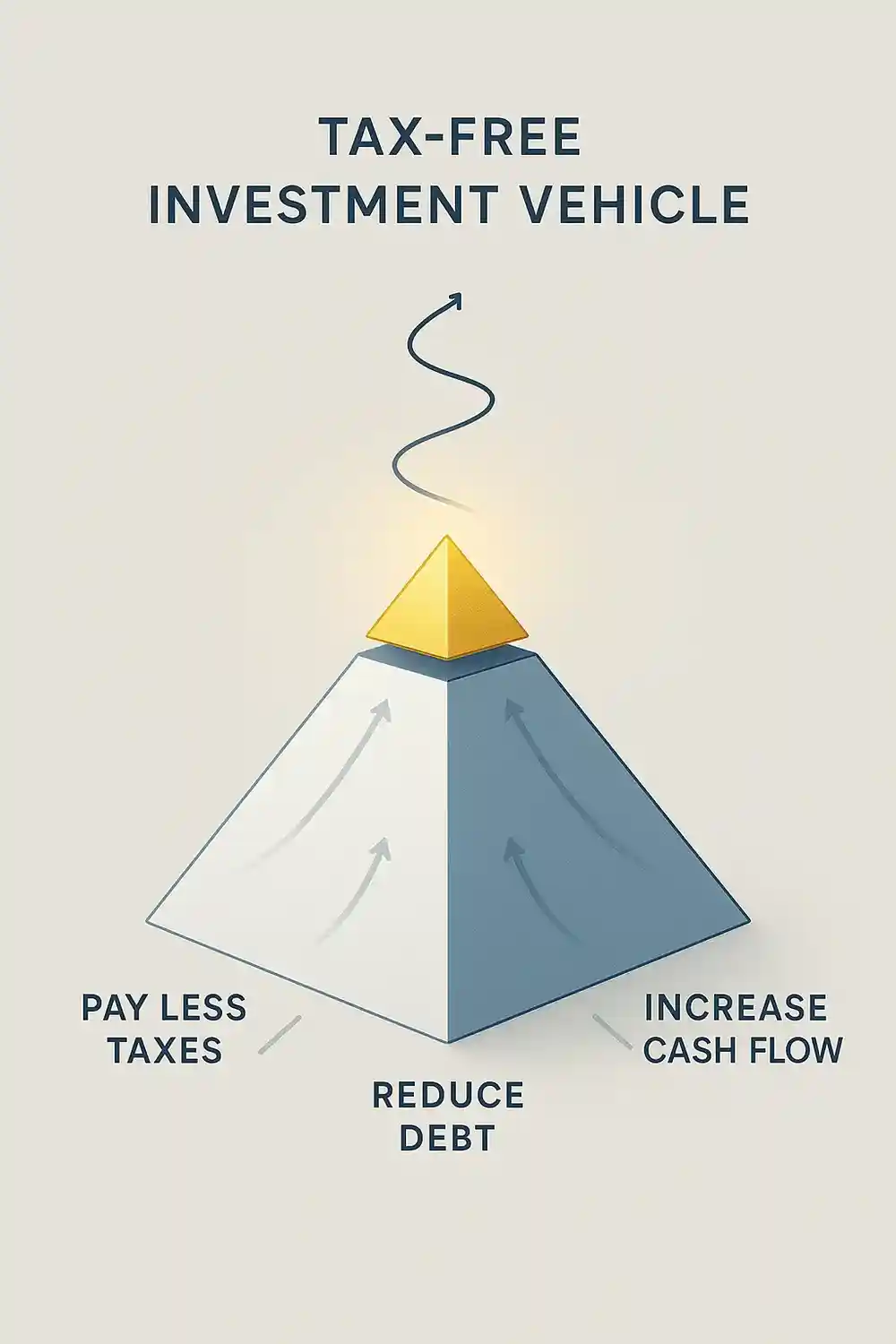

I've broken wealth building into 5 specific pillars that stack on each other. Most people try to do everything at once and end up doing nothing.

This framework gives you the exact order of operations - which moves to make first, second, and third.

At the base, you cut taxes legally so you keep 50-70% more of what you already earn.

After that, you eliminate high-interest debt so your money stops bleeding out every month.

Then, create income streams that grow without putting in more hours.

Use investment vehicles that grow tax-free and compound over time.

And finally, you protect it all through the right entity structures so you can pass it across generations!

This Way, It's Realistic For Anyone To Add

to your net worth in 12 months

(Most students end up adding much more... but $100K is the baseline we aim for)

The Challenge

The Middle-Class Money Trap: Why Working Harder Isn't Making You Richer

Why Your 401(k) Is Bleeding Money & What To Do Instead

Debt Elimination & Credit Mastery

Entity Structure & Business Credit Expert Deep Dive

Roundtable Q&A with Preston

The W-2 Taxes Playbook: Stop Losing Half Your Income

The Investor Playbook: Build Wealth Without Paying Taxes

100% Tax-Free Airbnb Business (No Property Required)

The Complete Wealth Acceleration System

Roundtable Q&A with Preston

Advanced Tax Optimization Expert Session

Your 12-Month Wealth Implementation Roadmap

How Students Hit $100K+ Net Worth (Real Numbers)

Your Next Steps and Beyond

Roundtable Q&A with Preston

March 20 - March 22, 2026

Starting From 10 AM EST | 4-6 Hours Daily

Streaming Online on Zoom

Join from anywhere. We'll send you a private link.

$100K+ Net Worth

Cut taxes, eliminate debt, build $5K-$15K monthly income.

Day 1 is about finding out where your money is really going, plugging the holes, and setting your path.

Most people think working harder and earning more equals building wealth, but they're stuck in a system designed to keep them middle-class forever.

The Trap:

You'll understand exactly why you feel broke despite good income and the mindset shifts that separate wealth builders from paycheck earners.

People think maxing out a 401(k) is the best move, but they don't realize it's designed to make Wall Street rich while you work for 40 years.

What's broken in their current approach:

We'll show you how to take control of when your money gets taxed and stop letting fund managers split your life savings with the IRS.

Most people think debt is something to avoid completely, but the wealthy use strategic leverage to buy assets that pay them.

Deepdive into strategies from industry experts who've helped tens of thousands of W-2 income earners & business owners optimize their financial structure and accelerate their wealth building timeline.

Watch Preston answer real attendee questions and strategy scenarios

Once the leaks are fixed, it's time to speed it up. Day 2 is about adding advanced strategies to boost your income and cut taxes to reach your goals faster.

How people making $1M+ pay less in taxes than someone making $80K. And how W-2 employees get punished for not knowing what business owners actually do.

What's broken:

Taxes are the #1 expense in life. High earners lose $1M+ over their lifetime due to poor structuring. You'll know exactly which strategies apply to your situation and how to implement them immediately.

Previous session is about defense: Keeping more of what you earn. This session is about offense: Building wealth that never gets taxed.

What's broken:

You'll learn how to write off major purchases, automatically reduce your tax bill on business income, turn investment losses into savings, and build wealth that compounds tax-free for decades.

I'll show you how to build income streams that net $5K-$15K monthly alongside your job and make it all tax-advantaged legally. Now that you've seen all the individual strategies, we'll show you how they work together as a complete system to add $100K+ to your net worth within 12 months.

Get clear implementation guidance for the most common strategy questions from this point in the training.

Watch Preston answer real attendee questions and strategy scenarios

The final step is making sure it lasts. Day 3 is about protecting what you've built, passing it on, and leaving a legacy that actually grows over time.

True wealth isn't just about making money. It's about keeping it and passing it on without getting taxed to death.

What's broken in their current approach:

We'll show you how to structure multi-generational wealth transfer the right way using the same legal structures the wealthy use.

The exact order to tackle each piece so you see results fast without getting overwhelmed. What to do first, second, and third to start building serious wealth immediately.

Real case studies from working professionals who implemented these exact strategies. See the specific numbers, timelines, and results so you know exactly what's possible.

Get final implementation direction and walk away knowing exactly what to do to add $100K to your net worth in the next 12 months.

Watch Preston answer real attendee questions and strategy scenarios

Why Attend This Challenge?

The Transformation

Starting From 10 AM EST | 4-6 Hours Daily

Join from anywhere. We'll send you a private link.

Cut taxes, eliminate debt, build $5K-$15K monthly income.

Choose Your Ticket

You'll walk away with a complete action plan:

Everything in General PLUS:

Everything in VIP, plus one extra benefit:

| Feature | General | VIP | Inner Circle |

|---|---|---|---|

| All 3 days of challenge training | ✓ | ✓ | ✓ |

| Recordings and replays of all sessions | — | ✓ | ✓ |

| All slides, notes & materials | — | ✓ | ✓ |

| Watch VIP Inner Circle Q&A sessions | — | ✓ | ✓ |

| Direct interactive Q&A with Preston | — | — | ✓ |

Proof It Works

"I didn't want to work my whole life just to be told I couldn't use my own money."

Dustin was in corporate sales, looking for a way out. The turning point came when his girlfriend's mom passed away at 62 with savings locked up. He decided to take his finances in his own hands.

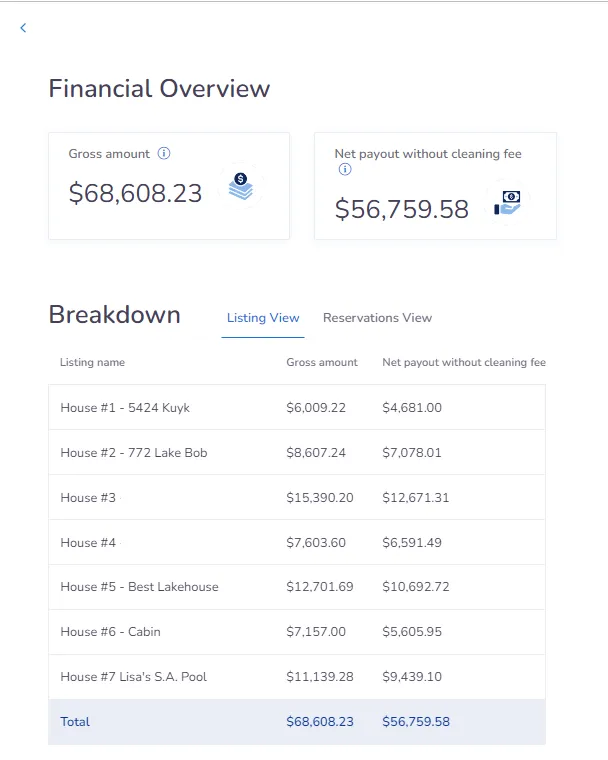

First property in 30 days, $3K/month

7 properties in under 2 years

$56K net profit in one month

Walked away from his 9 to 5

Turning Taxes Into Cash Flow and Long-Term Growth

Before, Galin was working hard but watching too much disappear to taxes and overhead. Now he has a plan to save big on taxes and add consistent rental income.

$100K+ in tax savings and paper losses

Six figures redirected into long-term investments

Estimated 12-Month ROI

~$150,000+

Eliminating Taxes and Building Early Freedom

Before, their household was stuck watching too much of a W-2 paycheck disappear to the IRS. Retirement felt locked away until age 59½, and every move seemed tied up with penalties or restrictions. After putting the right pieces in place, they now have a plan to legally cut taxes to zero, create penalty-free income years earlier, and move money into assets that actually grow.

~$52,500 cash refund from tax savings

$30K shifted into 0% tax brackets

Six-figure savings sheltered through new structures

New cash flow and long-term growth layered on top

Estimated 12-Month ROI

$50K-$100K

About Preston

I'm a 33-year-old who used to follow the same money rules as everyone else - save what's left, avoid debt, hope the 401k works out.

I was stuck in that cycle until I started learning everything I could about personal finance, investing, and real estate. My wife and I both applied what we learned. By 28, I became financially free and we built a $20M+ real estate portfolio.

I share what I've learned with over 6 million people about how money actually works and the real strategies wealthy people use.

Over the years, this work has put me in rooms with people like Pace Morby and Dean Graziosi. I've been featured alongside Ray Dalio, Robert Kiyosaki, and Daymond John.

No Questions Asked

We're confident that in just 3 days you'll walk away with a real plan to finally take control of your money.

If you don't leave with total clarity on what to do next, just email us within 7 days and we'll refund you.

Got Questions?

The Reality

Every month you delay = unnecessary taxes paid

Every month you delay = interest charges

Every month you delay = income missed

Every year you delay = future wealth lost

Total Cost of Waiting One Year

Here's the math: $4K/month in avoidable taxes ($48K/year) + $1K/month in unnecessary interest ($12K/year) + $10K/month in missed income opportunities ($120K/year) + $70K+ in lost compound growth = $250K+ every year you wait

Or you can invest $47 today and start keeping that money instead.

Mar 20th - Mar 22nd | 10 AM - 4 PM EST